- By: HomeEquity Bank

Could it possibly be a problem to suit your subscribers meet up with their old age income means? Since the rising cost of living continues to consume out from the discounts, your prospects may find it tough to availability brand new cash flow they need certainly to alive the wished lifetime. You to virtue one to resigned Canadians provides try home ownership. Actually, nearly 70% off Canadians individual their unique house, predicated on Re/Maximum. Opening some of you to definitely domestic security might help provide the cashflow customers you want.

Plus they don’t have to start making notice money up until they withdraw funds from the credit line account

Take out an effective HELOC. HELOC lenders generally make it homeowners to view as much as 65% of your worth of their homes. Customers is also borrow cash because they want to buy (to brand new decided amount) and are usually just expected to make lowest month-to-month interest payments on extent they will have taken out. Instead of home financing, there are not any scheduled costs into loan’s dominating; consumers will pay from the line of credit when it’s simpler in their eyes. Cost are typically below for other lines of credit as the borrowed funds is actually covered by the consumer’s household.

Rating an other mortgage. Additional method for homeowners to view the new security in their property is by using a face-to-face mortgage. This new Processor chip Opposite Home loan by HomeEquity Lender lets Canadian residents many years 55+ to access around 55% of its residence’s worth and turn into it on income tax-totally free cash without the need to circulate or sell. There are not any monthly home loan repayments making if you find yourself payday loan Pelham your web visitors live-in their homes; a full count just becomes owed once they move otherwise sell their property otherwise by way of its property once they perish.

People is get the finance as the a lump sum payment or even in regular month-to-month dumps. They’re able to use the dollars when it comes to financial need, and health care will cost you, house renos, debt consolidation or lives expenses.

Some of the trick advantages of an effective HELOC are their cosmetics and you may benefits. A great HELOC are a rotating personal line of credit, which means once your customers are recognized towards the collection of borrowing from the bank, they can availability bucks as required. An additional benefit would be the fact when you start to spend on the prominent, the quantity you can borrow of a great HELOC grows towards the completely new credit limit, getting proceeded usage of income.

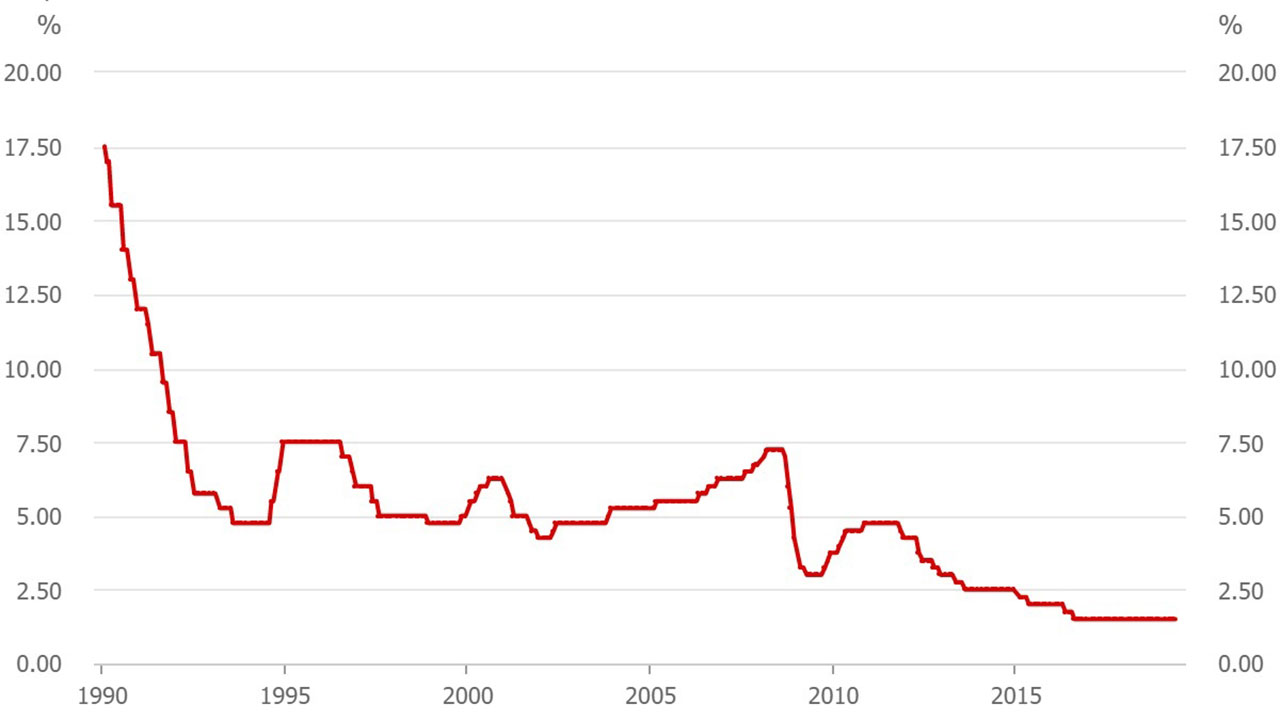

Up until now, probably the biggest benefit of good HELOC as compared to an other home loan is its lower interest rate. At the conclusion of 2022, the typical HELOC rates was about 2% less than the typical opposite home loan rates. But not, brand new pit between them prices have slimmed. In fact, the Processor Contrary Home loan 5-season Special Price was slightly less than the typical HELOC price in early .

One of the biggest benefits of this new Processor chip Reverse Financial try that we now have no month-to-month mortgage repayments something which helps make a distinction towards clients’ life, especially in the present day economic climate in which income is a problem. Listed below are some of the almost every other benefits of the new Processor Opposite Mortgage.

- Simplistic underwriting. Opposite mortgages are especially available for Canadians 55+ who are to your a predetermined money and may have difficulties being qualified to possess good HELOC.

- You should not requalify. An everyday HELOC regarding a lender will get subject the brand new borrower to help you continuous credit score monitors over time, impacting their ability to access a beneficial HELOC if needed.

- Loss of a spouse will not effect an opposing home loan. With a HELOC, new loss of a partner get produce the lending company to examine the financing get of the surviving companion.

- The reverse home loan has repaired-label price alternatives and will become locked in for to a great five-seasons name. Conversely, the prime financing rates out-of good HELOC tend to float, since it is linked with the financial institution from Canada’s finest price. While the we’ve got seen has just, this may improve borrowing costs from inside the a rising rate of interest ecosystem.

To have clients who would like to stay in their houses with no in order to downsize, property equity personal line of credit (HELOC) and you can an opposite home loan are a couple of of the very prominent implies to get into their property security

Another important factor to keep in mind would be the fact HELOC loans can expand rather over the years in case your members don’t pursue a typical percentage bundle.

Ready to help your web visitors make use of their home guarantee that have the fresh new Processor chip Contrary Financial? Visit us on the web to find out more, or get in touch with a business Innovation Director today.